The bond market is sending some important signals for anyone watching mortgage rates. Here is the breakdown as of this week.

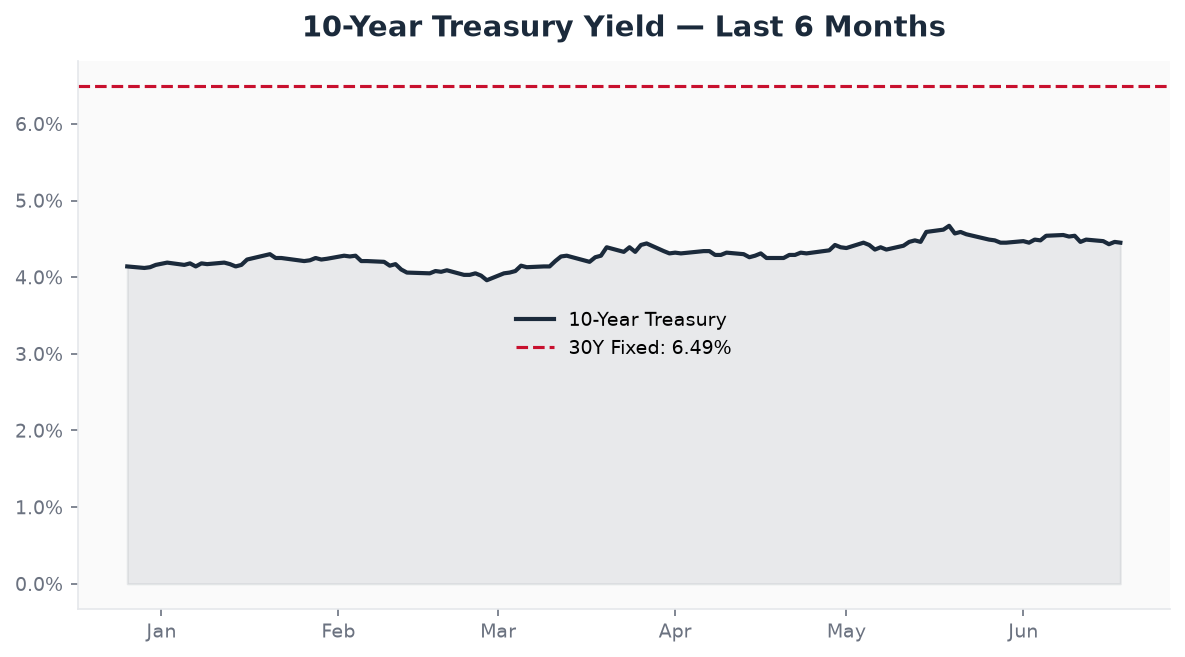

10-Year Treasury Yield — Last 6 Months

The 10-Year Treasury yield has been the anchor for mortgage rate movements over the past six months. Watching the trend line against the 30-year fixed mortgage rate overlay gives you a clear picture of where rates are headed.

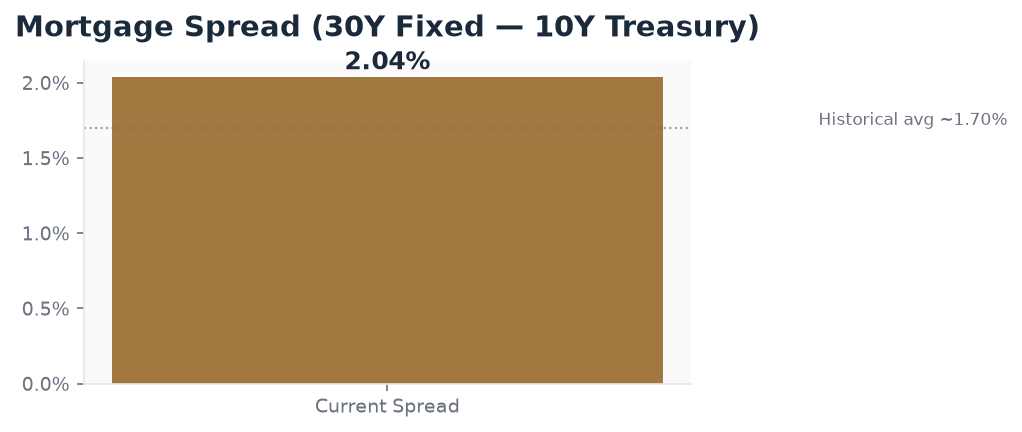

Mortgage Spread (30Y Fixed — 10Y Treasury)

Here is the part most people miss. The spread between the 10-Year Treasury and the actual 30-year mortgage rate is where lenders factor in risk, prepayment uncertainty, and operational costs. When this spread widens, mortgage rates climb faster than Treasuries — and that has been the story for much of this year. The historical average sits around 1.70%. When the current spread exceeds that, borrowers are paying a premium beyond what bond market movements alone would explain.

Fed Watch: What Markets Are Pricing In

The Fed just wrapped up their June meeting and held rates steady. Markets are now pricing in what comes next — the probability of cuts, holds, or hikes at upcoming FOMC meetings. These probabilities shift weekly based on economic data releases and Fed commentary. Watching the FedWatch tool gives you a forward-looking view of where short-term rates are headed, which ultimately influences mortgage pricing across the curve.

What This Means for Homebuyers

If you are shopping for a home in the West Metro or considering a refinance, here is what to watch: the 10-Year Treasury yield trend and the mortgage spread. When the spread normalizes back toward historical levels, that is when we typically see the most favorable mortgage pricing. Right now, locking in a rate when the spread is elevated means you are paying for more than just the Fed’s policy — you are paying for ongoing market uncertainty. That dynamic will shift as economic data clarifies and the Fed’s path becomes more predictable.

I track these numbers weekly and share what they mean for Twin Cities homebuyers and homeowners. If you have questions about how today’s rates affect your specific situation, call or text me at 952-994-4451.